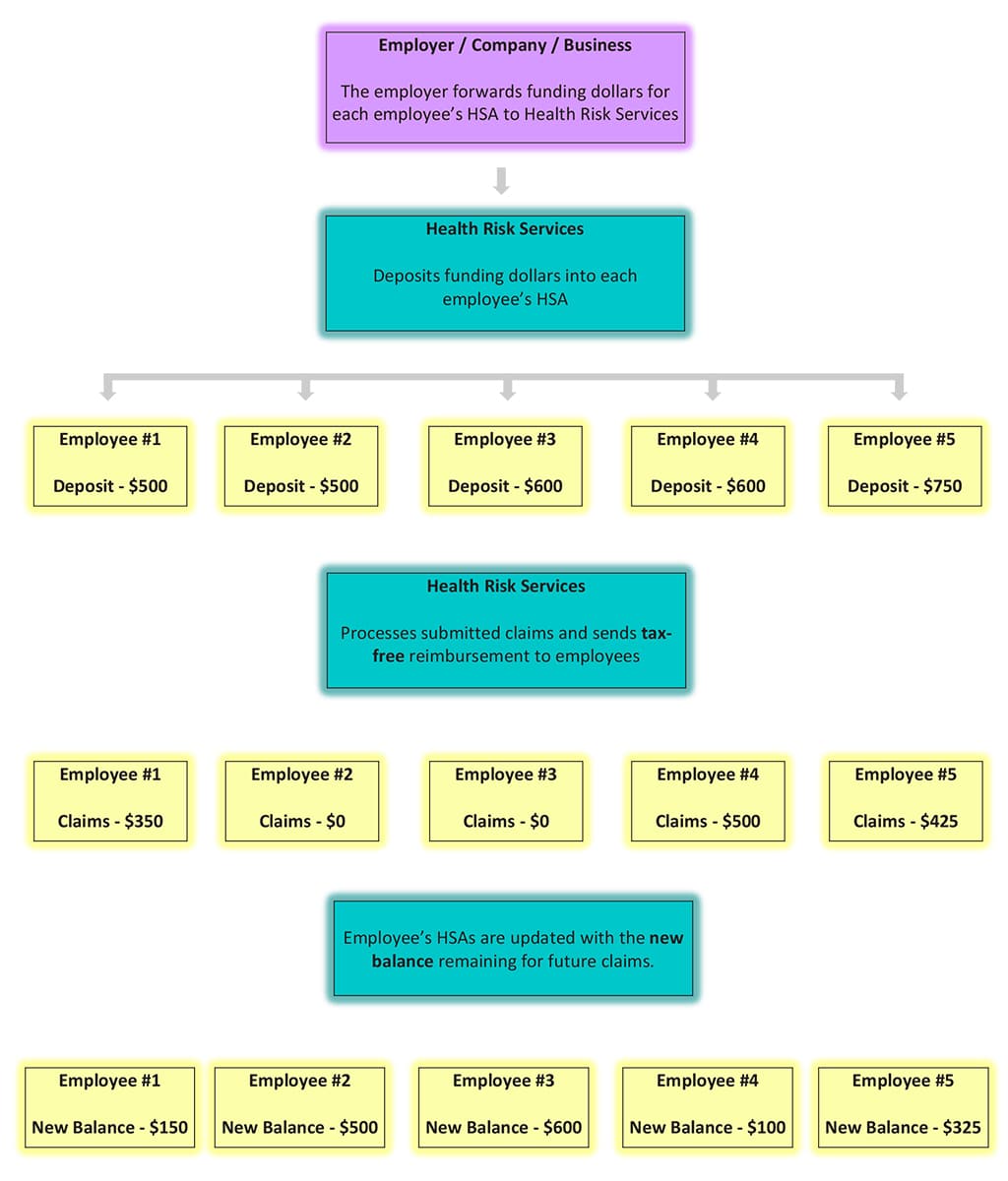

An HSA resembles a personal bank account as it works with debits and credits. With a positive account balance, an individual may obtain reimbursement for eligible medical and dental expenses and the account is debited by the paid amount. The amount deposited into each account must be used within a specified period (1 or 2 years), after which an unused balance is forfeited. This “use it or lose it” principle is required by Revenue Canada for the HSA to qualify as a private health services plan and is necessary to maintain a reasonable element of risk in the benefit plan for insurers.

Administration and Funding of a Health Spending Account (HSA)

There are three main areas of consideration when implementing an HSA – Philosophy, Carry Forward and Funding.

Philosophy: Should the company have a program that has a tiered benefit structure for different groups of employees in the organization? HSAs could be structured based on seniority or position within a company such as different benefit amount for executives, management and all other employees.

Carry Forward: The design of an HSA is determined by the method of “carry forward” that is selected by an employer. There are three options by which an HSA is constructed:

Balance Carry Forward – employees may roll over any accumulated credits in year one to year two. Any remaining balance would revert to the employer.

Expense Carry Forward – unused credit from year one may be carried over into year two. Any remaining balance of credits would revert to the employer at the end of year two.

No Carry Forward – employees can claim their expenses against employer credits within the year that the expense is incurred.

Funding: the employer’s pre-determined contribution amount can be allocated to fund an employee’s HSA in one of the following options:

Monthly. The employer will pay an equal amount each month.

Pay-As-You-Go. The employer pays an amount equal to the total of the claim and any expenses each month.

Annually. The employer will contribute a lump sum to all HSAs on a specified date once per calendar year.

Pro-Rated. The employer will pay monthly on an HSA that is actually being funded on a quarterly and semi-annual basis.

An HSA provides coverage to enable employees to meet their specific needs over and above a basic insurance plan for catastrophic coverage

Employers can budget more accurately for the cost of allocating set amounts each year for an HSA for each employee

Health and Dental claims are completely controlled by the HSA preset maximum for each employee

Employees aware of HSA maximum amounts will increase utilization to ensure use of all HSA account dollars

Overall costs of HSA may increase as employees use credits for their specific needs as opposed to a traditional plan which may only be used for certain needs of each employee

Taxability Status of a Health Spending Account

Certain criteria must be met for an HSA to be considered a tax-deductible business expense, the same as a traditional benefit plan.

HSAs must be 100% funded through employer contributions set prior to the benefit year (i.e. a set amount per person per year)

HSA funds cannot be used to purchase additional insurance (i.e. Life Insurance, Long Term Disability)

The amount of reimbursement is limited to the amount allocated to the account by the employer

Benefits must meet Canada Revenue Agency’s definitions of eligible expenses

Unused amounts in the HSA cannot be paid out at year end as cash to the employee

Qualifications

Incorporated business, limited companies or self-employed individuals and their families are eligible for HSAs. Claims may be submitted for eligible expenses which are incurred by an eligible employee, their spouse or any other dependent for which the employee is claiming a tax deduction in the taxation year the expense was incurred.